|

Excess Returns |

||

|

Insights for Investment Marketing and Sales Professionals |

|

How Active Managers Can Be More Active | February 2025 A long-term view. Buy and hold. Forever stocks … Almost all active asset managers, when asked about their competitive advantage, will use passive-sounding, undifferentiated language like this. A new issue of Excess Returns considers how active managers can communicate—and act—with greater distinction, vitality and precision. With best wishes, |

In This Issue Alpha Partners is an investment marketing firm specializing in custom research, marketing communications and presentation coaching. Our goal is to create alpha (excess returns) by helping investment firms win, keep and diversify assets under management. Alpha Partners LLC |

|

The Fullness of Time Heading into a meeting with a portfolio manager at a large, well-known investment firm, the marketing communications director gives me an earnest warning: “Whatever you do, don’t ask him about the sell discipline.” Puzzled, I ask “Why not?” Only to be told, “He just really doesn’t like talking about it.” During an in-depth background interview, I ask another portfolio manager, “What do you mean by ‘long term,’ or ‘over a full market cycle?’” “Oh, you know,” he says, “In the fullness of time.” How biblical, I think. He never did provide a true answer. Thinking about it later, I concluded that he was being dismissive. Or making fun of my question. Or both. I used to think of “long-term” as a desirable attribute resonant with positive meaning. But weirdly, in the investment world, through lack of clarity and vast overuse, claims of “a long-term perspective” have come to mean almost nothing. Ask investment managers to describe what distinguishes their strategy and virtually every company everywhere all the time will claim “a long-term outlook.” And this is true across asset classes. New Ways to Measure Active Manager Skill |

|

Learning from experience is one of the most powerful, constructive ways to be active in managing portfolios. Active managers today can improve systematically based on rigorous new measures of manager skill. |

|

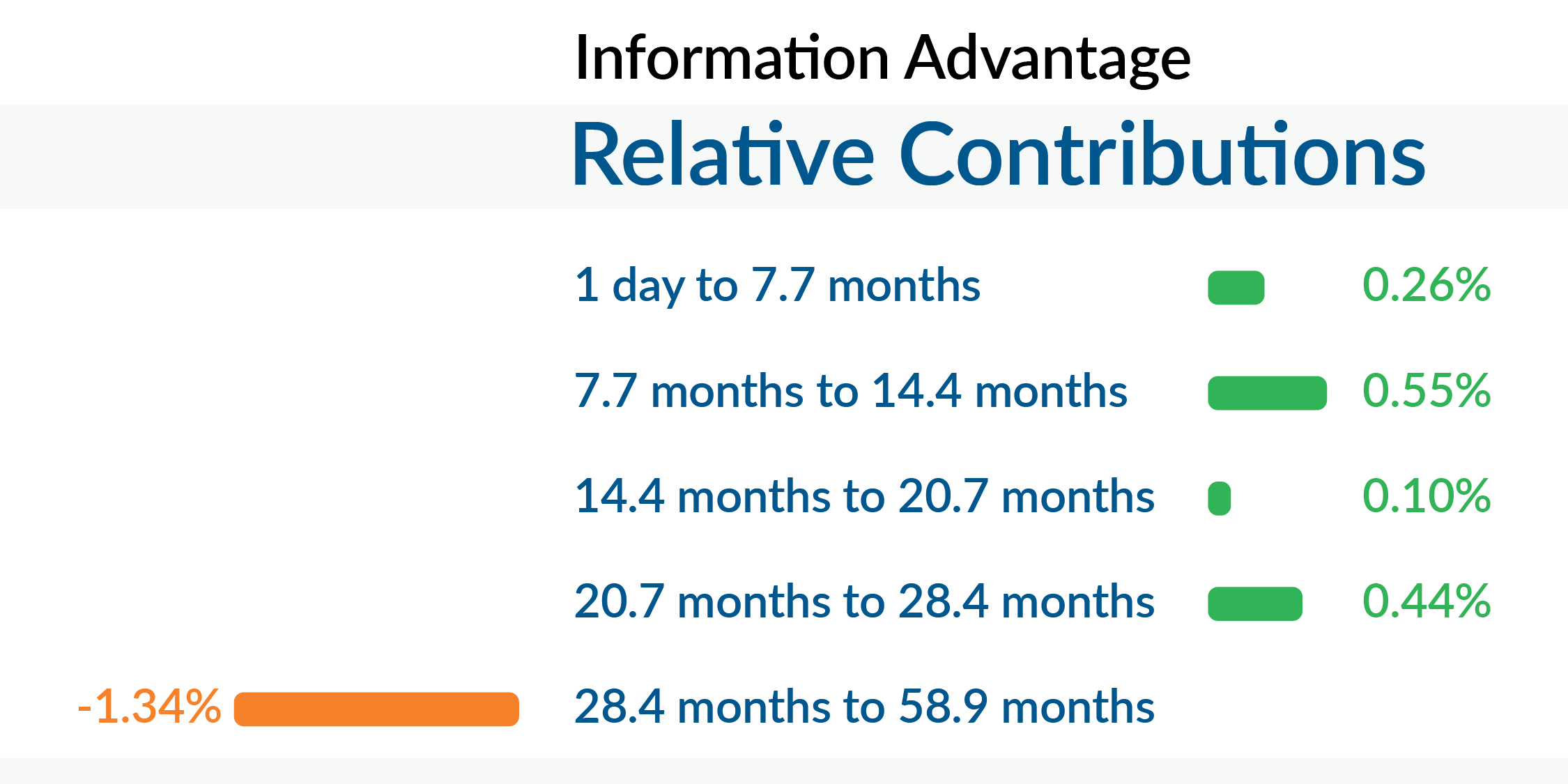

In reality, a long-term outlook truly is a competitive advantage. Short-term behaviors create opportunities for long-term investors every single day. And unhealthy public market pressure to perform in the short term is one of the reasons why private markets are becoming increasingly popular as a source of capital. So how does an investment firm present this genuine competitive advantage without sounding exactly like every other investment firm? And, bigger picture, how do long-term-oriented active managers do a better job of sounding active? Here are several suggestions: Be precise. Define your investment time horizon and what you mean by “a full market cycle.” Point to average annual portfolio turnover as evidence of a long-term mindset. (There are portfolio management teams claiming a long-term outlook with average annual portfolio turnover of close to 100%.) Note the number and age of long-term holdings and describe them, including case studies showing thoughtful patience when times are tough. Provide a few sector- and security-specific examples demonstrating the opposite of long-term behavior. Show that you know how to sell. Sometimes it’s easy to detect when a portfolio manager doesn’t know how to sell. Unwillingness to discuss the sell discipline and glib, evasive answers to related questions are one tip-off. Another is hanging a company’s identity on the cliché of long-term investing without any of the precision noted above. In a world increasingly dominated by index funds, passive-sounding “buy-and-hold,” expensive beta-masquerading-as-alpha strategies are more subject to challenge. Even so-called “forever stocks” sometimes need to be sold or trimmed. Demonstrate learning from experience. A particularly pernicious form of passivity is refusing to learn from experience. Learning from experience is one of the most powerful, constructive ways to be active in managing portfolios. And yet, according to Michael A. Ervolini, many investment managers remain impervious to improvement. Mr. Ervolini is the founder of Cabot Investment Technology, Inc., a global software company providing analytics to help money managers improve portfolio performance. FactSet bought Cabot in 2021, and until recently Mr. Ervolini served as a distinguished fellow at the company. His book, Managing Equity Portfolios: A Behavioral Approach to Improving Skills and Investment Processes, explores new ways to measure skill versus luck, helping investment managers gain a deeper understanding of their strengths and shortcomings.1 Based on in-depth discussions with more than 1,000 equity professionals, Mr. Ervolini has concluded that the industry is “bogged down in denial … more comfortable rationalizing lackluster results than tackling opportunities for deliberate improvement.” He sees such denial expressed in an unwillingness to even try new metrics designed to help managers “improve while more effectively describing their differentiated value.”2 One such metric is vintage analysis defined in brief here. According to Mr. Ervolini, here is what denial sounds like: “We already do that.” “We’re different. Those analytics don’t fit the way we do things here.” “That’s interesting, but right now we’re busy [doing something completely unrelated to improving].” “How do I know I won’t break something that’s already working?” “It makes total sense, but I can’t get my managers to buy into this sort of stuff.” Seriously? In an industry driven by performance measurement, these practitioners reject new ways of measuring how to improve performance? Why actively court change and new ways of getting better when you can continue hiding behind truisms such as “buy and hold?” But hiding is getting harder every day. “Although asset managers have been slow to embrace” needed changes, writes Mr. Ervolini, “their clients, asset owners/allocators, are exhibiting a much more favorable response to integrating new metrics in their decision processes … Among the many benefits derived from the new metrics is that asset owners/allocators are now able to confirm that the way a fund is being managed is consistent with its prospectus and marketing materials.” The phrase “in the fullness of time,” I have learned, “encapsulates the idea of God’s perfect timing … how He orchestrates events to align with His divine plan.”3 In colloquial terms, “in the fullness of time” means: “Eventually, if you wait long enough.” Yeah, I’m pretty sure that portfolio manager was being dismissive and mocking my question! Vintage Analysis Pioneered by Cabot-FactSet, vintage analysis is another way to measure a portfolio manager’s information advantage or access to information not already priced into the market. As shown below, vintage analysis offers a variation of contribution analysis showing contribution to returns based on position age sorted by quintile. |

Source: FactSet Research Systems, Inc. Permission provided by FactSet Research Systems, Inc. and Copyright FactSet Research Systems, Inc. |

|

|

This example demonstrates the information advantage of a fundamental global growth equity fund over the most recent three-year time period. This is a successful fund, having delivered over 150 basis points of relative return annually for the past decade. The contribution by age is positive (green) for four out of five quintiles with 10 to 55 basis points annually of relative contribution. The fifth or oldest quintile (red) was a drag on the fund, generating negative 134 basis points of relative contribution. The chart provides guidance on when a portfolio manager should start challenging positions. Results, however, are not always this easy to interpret, sometimes requiring additional metrics evaluating the information advantage by year as well as by sector and factor. Combining information advantage by position age with other new portfolio metrics also can be advantageous. New metrics include rigorous measures of individual skills (buying, selling and sizing) and deep loss evaluation (is there a need for a stop loss?). A modest but growing number of active fund managers, writes Mr. Ervolini, are using these and other metrics to evaluate the efficacy of selling younger and older positions.4 |

|

When “Timing, we believe, is an art. I will show that timing is really a science.” Operating in the investment world, where perfect timing is thought to be unattainable bordering on nonexistent, When: The Scientific Secrets of Perfect Timing is a joy to read. “To unearth the hidden science of timing,” author Daniel H. Pink and his researchers uncover insights about time and timing based on more than 700 studies in the fields of economics and anesthesiology, anthropology and endocrinology, chronobiology and social psychology. Read When to learn when it’s best to schedule earnings calls and surgery (in the morning), when to present bad news (before good news) and when to do one’s best work (for most of us, before noon without distractions and with deliberate breaks to enhance productivity). The book also provides inspiring examples of perfect timing among groups working in unison (singing in a choir, rowing crew). A blend of theory with practical advice, When offers invaluable guidance on how to configure our daily lives. |

|

|

1.For more on Mr. Ervolini’s work, visit skillversusluck.com. 2.“Weak Feedback and Denial Are Killing Active Management: A Slow Death, Perhaps, but One that Is Avoidable,” by Michael A. Ervolini, 3.BibleAsk. 4.For a more in-depth description of vintage analysis, see The Journal of Portfolio Management article noted in Footnote 2 immediately above. |

April 2025

Slashed spending by CEOs. Postponed or canceled construction projects. Jobs being cut and delays in hiring. “The unpredictability of President Trump’s stop-start trade offensive,” The Wall Street Journal noted on April 28, “is paralyzing companies on every front except one―taking an ax to costs.” Where will it all end? No one can know. And that’s why now is a very good time to read a book about the art of uncertainty. Professor David Spiegelhalter helps readers understand how humans have learned to measure, manage and survive the unknown. In addition to key insights about putting uncertainty into numbers, the author provides valuable lessons in successful strategies for communicating uncertainty.

January 2025

Income. Compound interest. Investments. Debt. Taxes, Inflation … All play a role in building a profitable life. But so do character traits such as stoicism, focus and making the most of present time. In The Algebra of Wealth, Scott Galloway, a marketing professor at NYU Stern School of Business and a serial entrepreneur, provides expert advice on how to generate income and turn income into wealth. Based on personal experience and behavioral research, Professor Galloway offers vital insights that transcend the typical personal finance book, covering topics such as the futility of worry, treating expense management as a “rational obsession” and finding one’s true identity through hard work as opposed to pursuing a passion.

October 2024

In this tale of Shakespearean proportions, Alok Sama describes his experiences working for one of the most prolific and audacious venture investment entities, SoftBank’s Vision Fund. Fund investments include ByteDance, Nvidia, Arm and Alibaba―along with legendary failures such as WeWork and Sam Bankman Fried’s FTX. At some point in his time as president and CFO of SoftBank, the author becomes aware of a plot to discredit him and a colleague―a plot involving surveillance of his family, a smear campaign in the press, bogus legal threats and even a honey trap. While hoping to learn who and why, the reader gets a fascinating crash course in early-stage tech investing.

August 2024

The Coming Wave describes how new technologies such as AI and synthetic biology are going to change the world. Not this year or next but over multiple decades. As a co-founder of two AI companies and the current head of AI at Microsoft, the author is well positioned to understand and communicate everything that can go right with the coming tsunami of new technologies―and everything that can go wrong. This book makes a compelling, heartfelt case for “claiming the benefits of the wave without being overwhelmed by its harms.”

February 2024

The devil is the potential for pandemics, climate change disasters, terrorist attacks and massive computer hacks. A leader in crisis management and homeland security, Juliette Kayyem documents in depth the perils of underreacting to the inevitable. By dismissing harbingers of doom as mere noise, countries and companies risk turning emergencies into calamities, local diseases into global pandemics and manageable negative events into existential crises. This book provides invaluable lessons on how to prepare for the devil, how to limit harm when the inevitable crises do occur and how to pivot in time for future disasters.

October 2023

The reality of war never goes away. “Once every couple of generations,” writes Barton Biggs in Wealth, War & Wisdom, “an epic event occurs that destroys accumulated wealth.” The U.S., Australia and Sweden “have been lucky―so far―but in Europe, the apocalypse has happened in one form or another on a regular, generational basis.” In addition to tracking the fascinating history of the markets during WW II, this book explores two primary enemies of wealth during war: complacency (it couldn’t happen here, not to us) and failure to diversify by country and asset class.

August 2023

The Price of Time: The Real Story of Interest

Destined to become a classic of economic history, Edward Chancellor’s book provides an intensively researched compendium of all the economic woes that can result from excessively low interest rates. Starting with the ancient origins of interest, the book moves to the unintended consequences of zero-bound (and even negative) interest rates, and concludes with the impact of ultra-low rates on emerging markets.

The Ivy Portfolio is an interesting and enjoyable read not only for investors but also for sales and marketing professionals who want to learn more about the university endowment market.

The Ivy Portfolio is an interesting and enjoyable read not only for investors but also for sales and marketing professionals who want to learn more about the university endowment market. “I’d be a bum on the street with a tin cup if the markets were always efficient.”

“I’d be a bum on the street with a tin cup if the markets were always efficient.”